Update: The GOP accelerated the timeline of their move to wash away the essential health benefit provision that Obamacare put in place in an effort to woo conservatives in the house who were apprehensive about Trumpcare. The CBO score mentioned in this post does not reflect the latest amendments, though an additional analysis of previous amendments came to similar conclusions (with regard to how many millions of people would lose coverage) as the first.

Republicans have tried to tie the words “freedom,” “choice,” and “access” to their healthcare plan with as much determination as they’ve tried to hang the words “failure” and “disaster” on Obamacare. But what kind of choice are they really trying to give you when it comes to how you buy health insurance? And what kind of coverage is really going to be available when the dust clears?

It’s hard to completely buy into Paul Ryan, Donald Trump, Tom Price, and the GOP’s depiction of Obamacare after hearing the success stories and eyeing the number of people that gained coverage thanks to the law and its subsidies. But if you don’t qualify for a subsidy, or you feel like you can’t access the benefits that you’re paying for because of a sky high deductible, then you’ve got reason to be angry. Just maybe not blindingly so.

A Flawed Plan

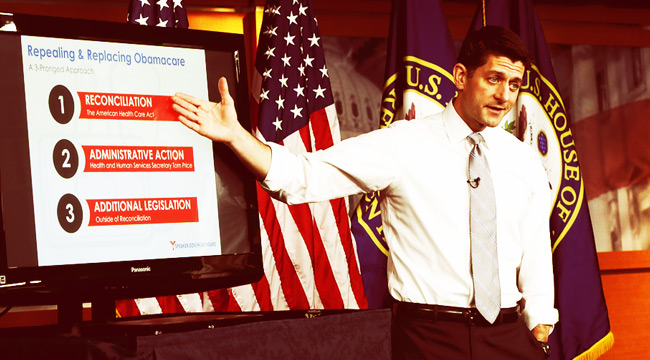

The GOP has relied upon that anger in the fight to repeal Obamacare and the gamble is that it will continue to be so strong that it will keep people from seeing the warts on a deeply flawed replacement plan that has, to this point, failed to garner the full support of a divided Republican party. And that effort got harder on March 13 when the non-partisan CBO’s analysis of Trumpcare indicated that it would cause 24 million fewer people to have insurance over a ten-year period while raising out-of-pocket costs.

According to The Hill, Paul Ryan’s response to this was to highlight the sunnier side of the CBO forecast like the nearly $350 billion in deficit reduction and the nominally lower premiums (on average, but not for the elderly, who will see an increase) that are expected to come into effect in 2020. (This after two more years of growth.) Ryan also leaned on the word “access” and the notion of freedom once again.

“I recognize and appreciate concerns about making sure people have access to coverage,” Ryan added. “[O]ur plan is not about forcing people to buy expensive, one-size-fits-all coverage. It is about giving people more choices and better access to a plan they want and can afford.”

To be fair, the 20-25% drop in insurance premium costs for the average 21-year-old in the individual market that is expected by 2026 is not nothing. That is unless you’re actually paying for next to nothing. And possibly paying for more of it out of pocket since the Trumpcare tax breaks aren’t tied to income (like the Obamacare subsidies are), but rather, age. Which means younger low-income Americans on the individual market could get less assistance if their plans were previously covered and cost more than the size of the $2,000 tax credit.

Access To What, Exactly?

Part of the GOP playbook is to roll back the essential health benefits that Obamacare lays out as a requirement for every metal (bronze, silver, gold) plan sold on the exchanges. They make their first move in the Trumpcare bill, but the Intercept reports that the plan is to more fully scrub the requirements (in phase 2 or phase 3) that have proven to be a thorn in the side of health insurance companies.

Rep. Kennedy confirms GOP health bill would remove essential benefits, incl. mental health, for Medicaid expansion enrollees—@EnergyCommerce pic.twitter.com/e40Ov6iEJ0

— Kyle Griffin (@kylegriffin1) March 9, 2017

Theoretically, this would allow insurers more freedom to offer a greater number of plans on the individual market with minimal benefits that people can then buy at a low cost across state lines. Or, because there wouldn’t be an individual mandate: not buy, exposing themselves to the risk of catastrophic medical debt and substandard care should they get sick. Because that’s what “freedom” looks like when it’s given to the insurance industry: an abundance of threadbare options for consumers who have no way of knowing what their health insurance needs are going to be in one year, one month, or one week. But if you’re in that camp where you feel like you’re bulletproof and you don’t need even these basic protections, please realize how goddamn expensive health care is when health insurance doesn’t cover essential benefits.

If you get into a car accident and wind up going to the ER or staying in a hospital for a few days, it’s entirely possible that your insurance might not cover the cost of your stay (which can soar into the tens of thousands) if the effort to erase those benefits proves successful. Think of what it would feel like to tack on another student-loan sized debt onto your life.

It costs $9,000 to $25,000 to have a baby in a hospital without coverage. If you need alcohol or drug rehab but can’t afford to pay the tens of thousands of dollars that in-patient care can run because your garbage insurance won’t cover it, how are you going to get the help you need? Same thing if you get diagnosed with diabetes and suddenly need insulin shots that have risen in cost to approximately $500 a month for some. Or blood tests to check your A1C every few months, since lab tests are an essential benefit presently.

Maybe some of these scenarios can be righted by departing a lesser plan for a more comprehensive one, but who knows how much those will cost if they become a comparative luxury. Remember, the insurance companies are governed by a profit motive, you’re governed by a survival motive, and these things don’t really mesh. Government is supposed to step in to make sure people don’t get steamrolled, but it feels like they’re driving the machinery this time around.

A Poor Fix

In his roundly-mocked Powerpoint presentation, Paul Ryan and his “regular Joe” forearms drew a line between the sick and the healthy and expressed dismay that the latter helps to offset the cost of the former. The line was off-the-mark since the Kaiser Foundation pegs the number of people with pre-existing conditions at about 27%, not whatever that small sliver on Ryan’s chart represented, but that’s not the point. The point is that Ryan doesn’t seem to understand how and why insurance works.

That targeted individual mandate is another Obamacare construct with problems. Namely, that it doesn’t come with a steep enough penalty to drive the young and healthy to the individual market when they don’t have any other real option to get insurance.

Ryan, Trump, Price, and the GOP are trying to kill the individual mandate with fire and sticks, but it theoretically brings balance to the process and has the ability to keep costs down across the board. Because the more people in the pool — specifically people that are going to pay their premiums and not use those services (while still being confident in the knowledge that they are there should they need them) — the better.

When you stop forcing people to make the right choice and you then offer them crappy insurance for not a lot less than what you were charging them before (but which may seem like a lot more since you’re cutting into the help they get), you give people no real incentive to buy health insurance. And it’s no real choice, either.

It’s funny, in an effort to create a soft landing for the dirigible crash that the GOP saw coming on the horizon with the CBO score, they tried to undermine the accuracy of that institution (another familiar song from the “believe me!” crowd). But really, you wonder how the CBO can accurately gauge to what extent people will look at the individual market, label it a dumpster fire, and move on if the benefits are lacking and the costs are still high. A move that would cause the ranks of the uninsured and prices to go even higher than the already bleak analysis predicts.

Actually, I take it back, it’s not that funny. It’s a bit frightening because political nonsense and ideological stubbornness have driven us all to this point. And now, to fix healthcare, we’re told that we have to kill the only thing that has made real progress in the fight. That is, replacing it with something that could strip consumer protections and do shockingly little to make real health care truly affordable.