The Big Short author Michael Lewis has a new podcast out called Against The Rules, and in the most recent episode he starts with the story of his recent hassle over an identity theft incident. Someone had apparently borrowed $16,000 in Lewis’s name with Citigroup, and he’d since been hounded by collectors at all hours of the day, watched his credit score plummet, navigated various call center hells with both Citigroup and Experian (one of the credit agencies responsible for reporting your debts to other banks) in an attempt to get it worked out, and finally ended up at the Berkeley police station, where he was advised to go to file a police report as a first step towards clearing up the matter.

Lewis’s is far from the first story about the nightmare of identity theft (and frankly it’s kind of obnoxious hearing him talk about how he’s never bought anything on credit) but in telling it, Lewis asks a basic question that few of these stories ever seem to: if a person Lewis doesn’t know, commits fraud against a bank Lewis has never had an account with, why is the burden of cleaning up the mess on him? Lewis’s identity theft story is a framing device. The larger question is about consumer banking, and the outsize control we’ve given this industry over so many foundational aspects of our lives.

The next chapter is the story of a teacher in the Bronx, who’s been paying off her $70 thousand plus in student loans for more than 10 years. There’s a program designed to forgive student loans for borrowers in public service professions exactly like this, provided they make 120 on-time payments. Which is to say, a perfect borrower record for 10 years, which isn’t easy. It was a measure pushed through in that brief political moment in the wake of the 2008 financial collapse when congress actually had to seem like they were trying to reign in the excesses of the financial industry and do something to help their constituents.

The teacher says she had to find out about the program on her own, because her servicer, Navient, never told her it existed. And when she finally did find out about it, she spent hours on the phone, talking to representatives, applying, and faxing forms back and forth, often being told they were missing certain information, until she was finally enrolled. Or so she thought. She was counting down the days to her final payment. Once the finish line was actually in sight, her servicer informed her that not only was the goal actually not in sight, she was never enrolled and never qualified in the first place.

Her story is not an anomaly. A later study found that of the more than 28,000 applicants for the program, only 96 had been approved, a rejection rate of almost 99.7%. Again, student loan horror stories are nothing new (an indictment in its own right), but Lewis gets to the most salient point: Navient’s complete lack of incentive to help borrowers navigate their loan options, despite that theoretically being the company’s only reason for existing.

Navient is just one of a handful of student loan “servicers.” The government loans students money through the Department of Education, who then outsource the management of that loan to private companies, who make a fee for each borrower. They “manage” the repayment options, which encompasses things like the public service loan forgiveness program that the teacher was applying for.

Those companies’ only real incentive is to keep making fees on each loan while devoting as little of their own resources to it as possible — an incentive Lewis shows manifesting from the top all the way down to the entry-level employee. He talks to a former Navient call center employee who describes being advised to try to limit calls with borrowers to less than seven minutes. She was also trained to spend most of the call verifying the caller’s identity, current address, account number, etc., before the caller could even get to the reason for their call, a strategy Lewis compares to “running out the clock” in pre-shot clock-era basketball. The call center employees who were best at getting borrowers off the phone the quickest were the ones most valuable to the company, and soonest in line for promotions and such. Notably, it wasn’t the employees who were most knowledgeable about repayment options or the best at helping customers find the best one for them.

And why would they be? The company’s incentive was only to push borrowers into whatever repayment plans would keep them on the rolls the longest. This is all logical behavior on the loan servicer’s part. The bigger question is one of public policy: why do servicers get taxpayer money for this? Why are we paying these loan servicing companies to perform at-best apathetic and most likely predatory “service?”

Navient is currently facing lawsuits brought by the Consumer Financial Protection Bureau, which was created by Elizabeth Warren to be for financial products what the Consumer Product Safety Commission is for things like kids’ toys and high chairs. One of the ways Warren campaigned for its existence was to present legislators with three credit card applications and ask them to try to figure out which one had the best interest rate

As you might imagine, the future of such protections doesn’t look good. The current head of the CFPB is acting Trump White House chief of staff Mick Mulvaney, a guy who got the job by arguing against the CFPB’s existence and whose signature moves as its head include: firing the entire advisory council, and trying to change the name to the “Bureau of Consumer Financial Protection,” which would’ve cost an estimated $300 million. Mulvaney is a constipated weasel of a man whose protection of the payday loan industry was recently profiled in the New York Times, though of course he’s not alone in protecting predatory industries. Joe Biden famously supported a bill that denied student loan borrowers bankruptcy protections. Meanwhile, Betsy Devos has issued a memo outlining plans to protect student loan servicers from any state laws attempting to reign them in.

{kind=link}

Which is, of course, no surprise coming from someone who has spent basically her entire “career” trying to divert money from public schools to private schools, through vouchers and other programs. Devos’s brother is Erik Prince, the founder of Blackwater, the private security force that was more or less founded on trying to privatize military operations. Which is to say, to earn taxpayer money to perform functions traditionally performed by government employees. Diverting public money to private enterprise is practically a religion among these people.

Obviously, student loans and military security are not the only sectors in which this dynamic, of the government paying private companies for their “public service” of extracting profit, plays itself out. Every time Bernie Sanders or other Democratic presidential candidates renew their call for Medicare for All, mainstream news outlets ready their shoutiest, most faux-skeptical headlines, all wondering some variation on “what will it cost, really?”

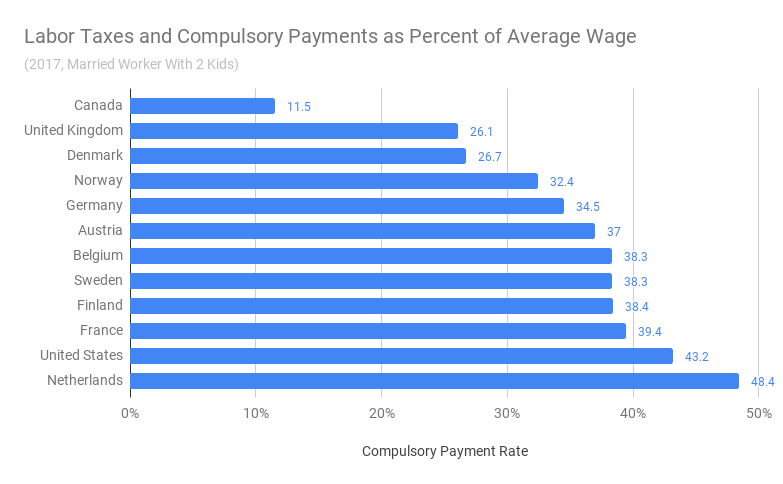

They almost always focus on what the direct cost to the government will be. Which conveniently ignores what Americans are already paying and where our money actually goes. We already pay a ton for healthcare, we just pay it in the form of employer payroll taxes and compulsory payments to private insurers extracted from wages. Matt Breunig at the PeoplesPolicyProject recently did a comparison of what American workers actually pay, once you include employer payroll taxes and insurance premiums, to other developed countries. Yep, we pay more. A lot more. Just compare what US workers pay to what our Canadian neighbors pay. And Canadians actually get health coverage for their money, without having to worry that changing jobs means they lose healthcare for them and their families.

{kind=link}

It’s a dynamic that seems to play out all over American life. We already pay, often in subtle ways where it’s not even obvious that the money is being extracted, and we don’t ask the private sector for anything in return. Health insurers don’t even have to follow antitrust laws. Our arbitrary and semantically flawed fear of “big government” has created and nurtured entire industries of predatory corporate middle men, charging us a fee for charging us fees. It’s madness.

Vince Mancini is on Twitter. You can find his archive of film reviews here.